Wealth distribution model

This model is a simple agent-based economy that is modelled according to the work of Dragulescu et al.. This work introduces statistical mechanics concepts to study wealth distributions. What we show here is also referred to as "Boltzmann wealth distribution" model.

This model has a version with and without space. The rules of the space-less game are quite simple:

- There is a pre-determined number of agents.

- All agents start with one unit of wealth.

- At every step an agent gives 1 unit of wealth (if they have it) to some other agent.

Even though this rule-set is simple, it can still recreate the basic properties of wealth distributions, e.g. power-laws distributions.

Core structures: space-less

We start by defining the Agent type and initializing the model.

using Agents, Random

@agent struct WealthAgent(NoSpaceAgent)

wealth::Int

endNotice that this agent does not have a pos field. That is okay, because there is no space structure to this example. We can also make a very simple AgentBasedModel for our model.

function wealth_model(; numagents = 100, initwealth = 1, seed = 5)

model = ABM(WealthAgent; agent_step!, scheduler = Schedulers.Randomly(),

rng = Xoshiro(seed))

for _ in 1:numagents

add_agent!(model, initwealth)

end

return model

endwealth_model (generic function with 1 method)The next step is to define the agent step function

function agent_step!(agent, model)

agent.wealth == 0 && return # do nothing

ragent = random_agent(model)

agent.wealth -= 1

ragent.wealth += 1

end

model = wealth_model()StandardABM with 100 agents of type WealthAgent

agents container: Dict

space: nothing (no spatial structure)

scheduler: Agents.Schedulers.RandomlyWe use random_agent as a convenient way to just grab a second agent. (this may return the same agent as agent, but we don't care in the long run)

Running the space-less model

Let's do some data collection, running a large model for a lot of time

N = 5

M = 2000

adata = [:wealth]

model = wealth_model(numagents = M)

data, _ = run!(model, N; adata)

data[(end-20):end, :]| Row | time | id | wealth |

|---|---|---|---|

| Int64 | Int64 | Int64 | |

| 1 | 5 | 1980 | 0 |

| 2 | 5 | 1981 | 2 |

| 3 | 5 | 1982 | 1 |

| 4 | 5 | 1983 | 0 |

| 5 | 5 | 1984 | 1 |

| 6 | 5 | 1985 | 2 |

| 7 | 5 | 1986 | 0 |

| 8 | 5 | 1987 | 0 |

| 9 | 5 | 1988 | 0 |

| 10 | 5 | 1989 | 1 |

| 11 | 5 | 1990 | 0 |

| 12 | 5 | 1991 | 0 |

| 13 | 5 | 1992 | 0 |

| 14 | 5 | 1993 | 1 |

| 15 | 5 | 1994 | 0 |

| 16 | 5 | 1995 | 0 |

| 17 | 5 | 1996 | 0 |

| 18 | 5 | 1997 | 1 |

| 19 | 5 | 1998 | 0 |

| 20 | 5 | 1999 | 0 |

| 21 | 5 | 2000 | 4 |

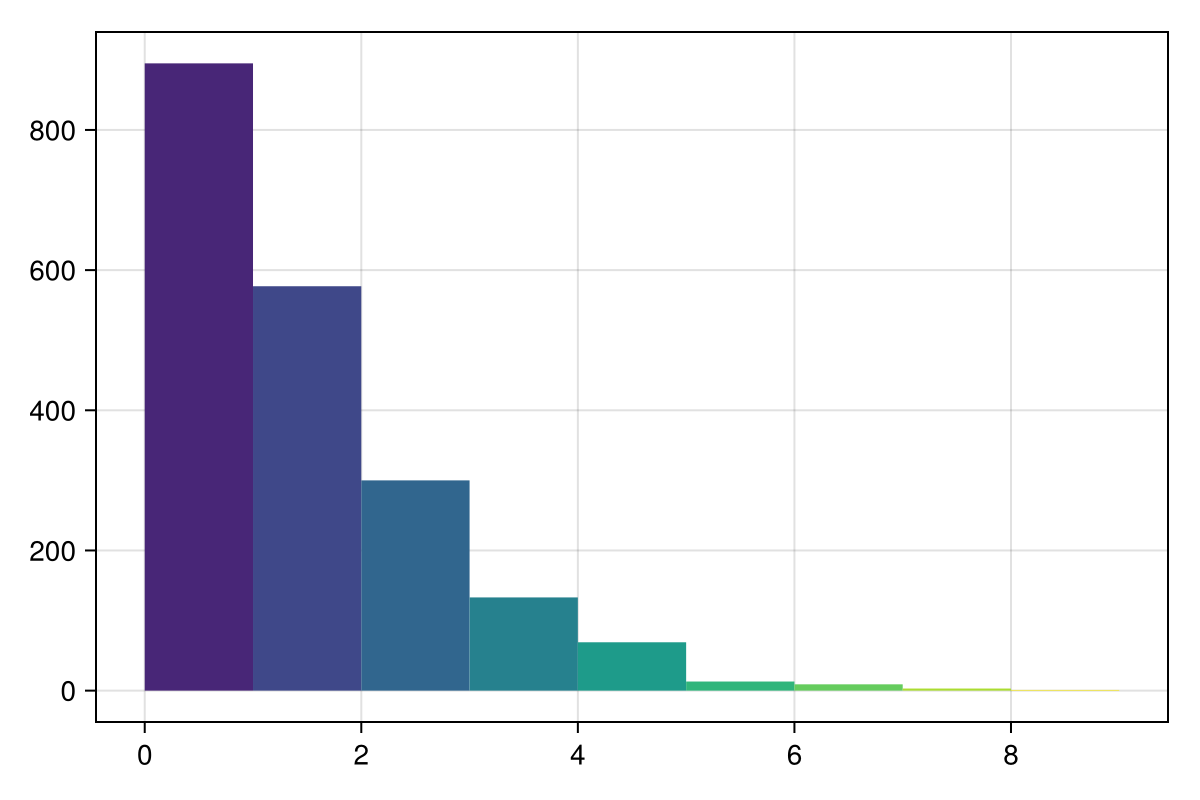

What we mostly care about is the distribution of wealth, which we can obtain for example by doing the following query:

wealths = filter(x -> x.time == N - 1, data)[!, :wealth]2000-element Vector{Int64}:

0

0

0

1

0

0

0

1

2

1

⋮

0

2

1

0

1

2

0

0

4and then we can make a histogram of the result. With a simple visualization we immediately see the power-law distribution:

using CairoMakie

hist(

wealths;

bins = collect(0:9),

width = 1,

color = cgrad(:viridis)[28:28:256],

figure = (size = (600, 400),),

)

Core structures: with space

We now expand this model to (in this case) a 2D grid. The rules are the same but agents exchange wealth only with their neighbors.

It is also available from the Models module as Models.wealth_distribution.

We therefore have to add a pos field as the second field of the agents:

@agent struct WealthInSpace(GridAgent{2})

wealth::Int

end

function wealth_model_2D(; dims = (25, 25), wealth = 1, M = 1000)

space = GridSpace(dims, periodic = true)

model = ABM(WealthInSpace, space; agent_step! = agent_step_2d!,

scheduler = Schedulers.Randomly())

for _ in 1:M # add agents in random positions

add_agent!(model, wealth)

end

return model

endwealth_model_2D (generic function with 1 method)The agent actions are a just a bit more complicated in this example. Now the agents can only give wealth to agents that exist on the same or neighboring positions (their "neighbors").

function agent_step_2d!(agent, model)

agent.wealth == 0 && return # do nothing

neighboring_positions = collect(nearby_positions(agent.pos, model))

push!(neighboring_positions, agent.pos) # also consider current position

rpos = rand(abmrng(model), neighboring_positions) # the position that we will exchange with

available_ids = ids_in_position(rpos, model)

if length(available_ids) > 0

random_neighbor_agent = model[rand(abmrng(model), available_ids)]

agent.wealth -= 1

random_neighbor_agent.wealth += 1

end

end

model2D = wealth_model_2D()StandardABM with 1000 agents of type WealthInSpace

agents container: Dict

space: GridSpace with size (25, 25), metric=chebyshev, periodic=true

scheduler: Agents.Schedulers.RandomlyRunning the model with space

init_wealth = 4

model = wealth_model_2D(; wealth = init_wealth)

adata = [:wealth, :pos]

data, _ = run!(model, 10; adata = adata, when = [1, 5, 9])

data[(end-20):end, :]| Row | time | id | wealth | pos |

|---|---|---|---|---|

| Int64 | Int64 | Int64 | Tuple… | |

| 1 | 9 | 980 | 9 | (9, 9) |

| 2 | 9 | 981 | 1 | (21, 24) |

| 3 | 9 | 982 | 11 | (3, 11) |

| 4 | 9 | 983 | 0 | (2, 18) |

| 5 | 9 | 984 | 0 | (22, 5) |

| 6 | 9 | 985 | 10 | (10, 2) |

| 7 | 9 | 986 | 1 | (3, 23) |

| 8 | 9 | 987 | 1 | (9, 2) |

| 9 | 9 | 988 | 3 | (13, 12) |

| 10 | 9 | 989 | 6 | (23, 3) |

| 11 | 9 | 990 | 7 | (25, 3) |

| 12 | 9 | 991 | 0 | (16, 1) |

| 13 | 9 | 992 | 8 | (20, 21) |

| 14 | 9 | 993 | 3 | (17, 15) |

| 15 | 9 | 994 | 5 | (16, 19) |

| 16 | 9 | 995 | 3 | (15, 10) |

| 17 | 9 | 996 | 3 | (14, 10) |

| 18 | 9 | 997 | 0 | (20, 6) |

| 19 | 9 | 998 | 1 | (12, 2) |

| 20 | 9 | 999 | 4 | (13, 18) |

| 21 | 9 | 1000 | 4 | (17, 10) |

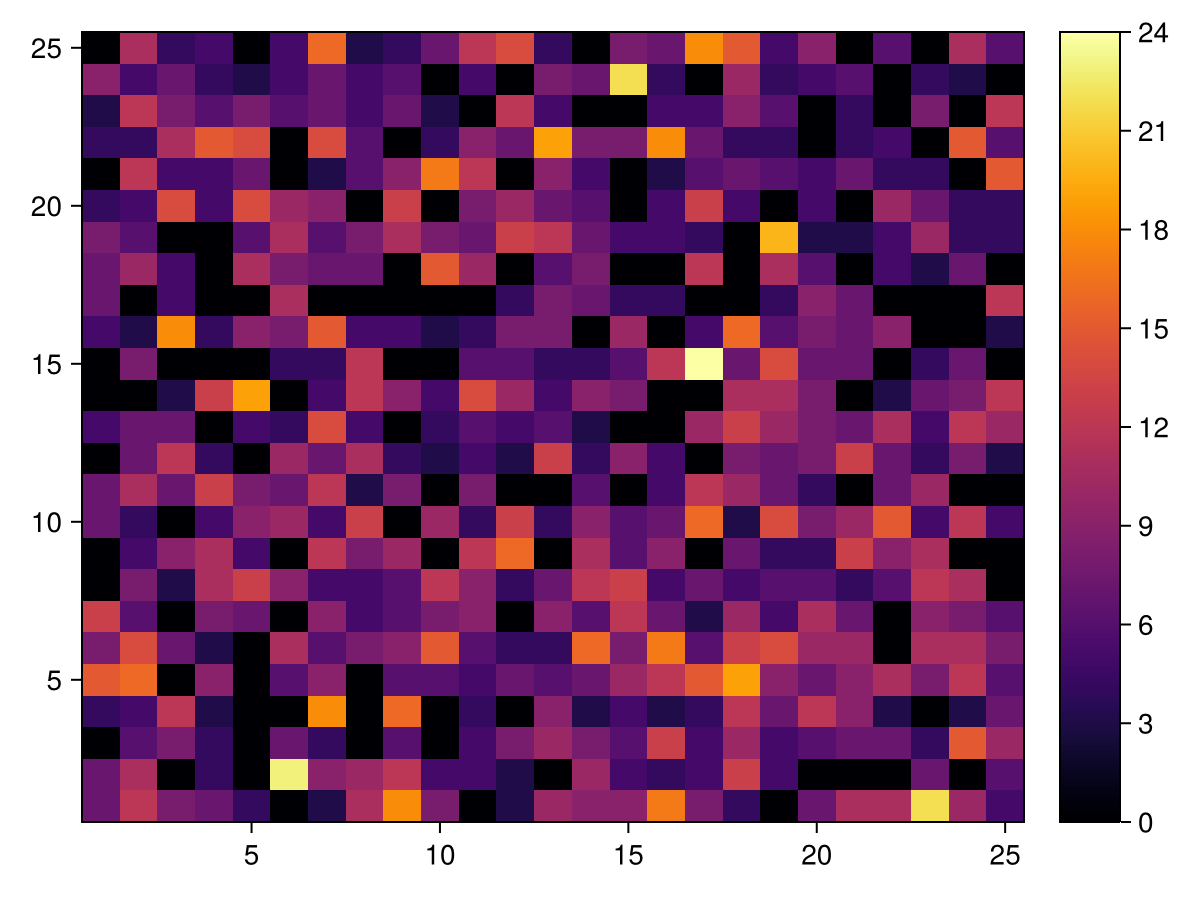

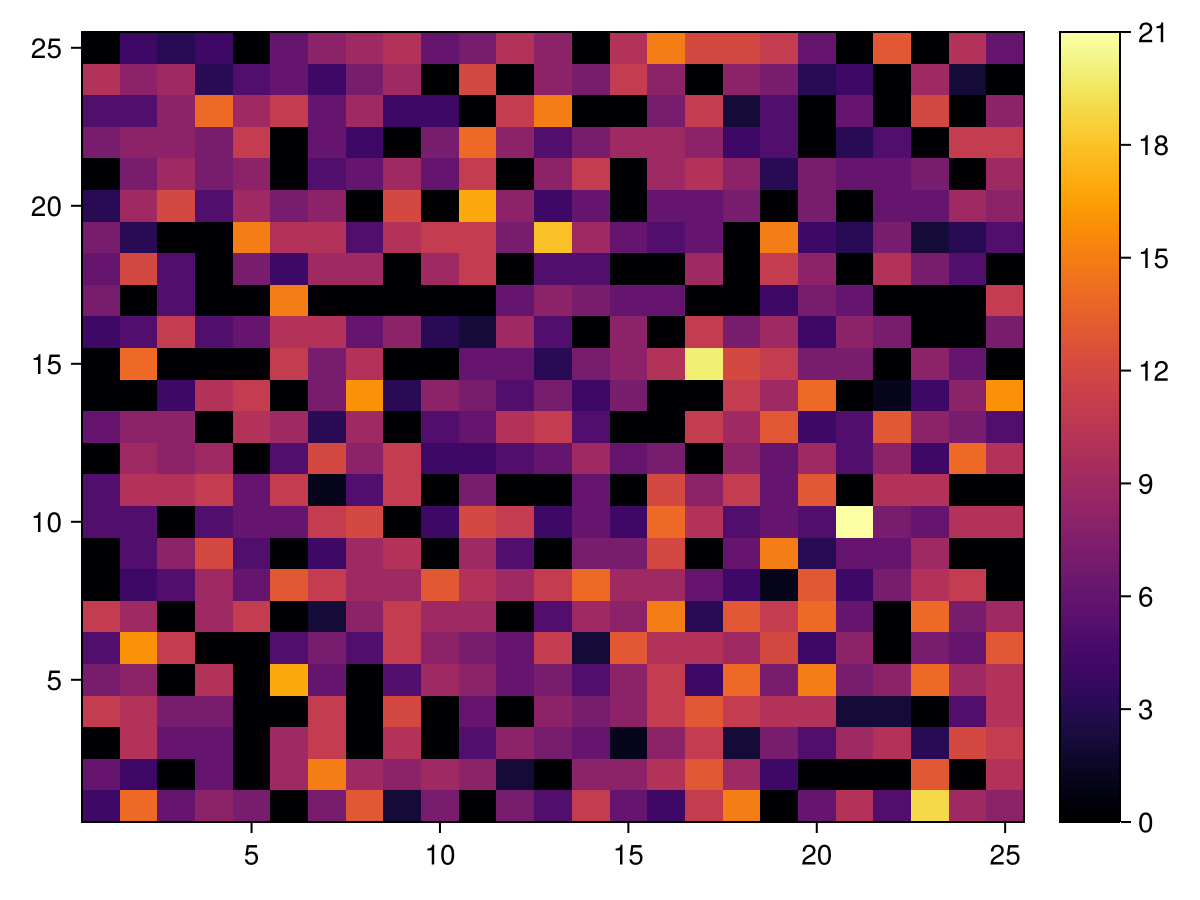

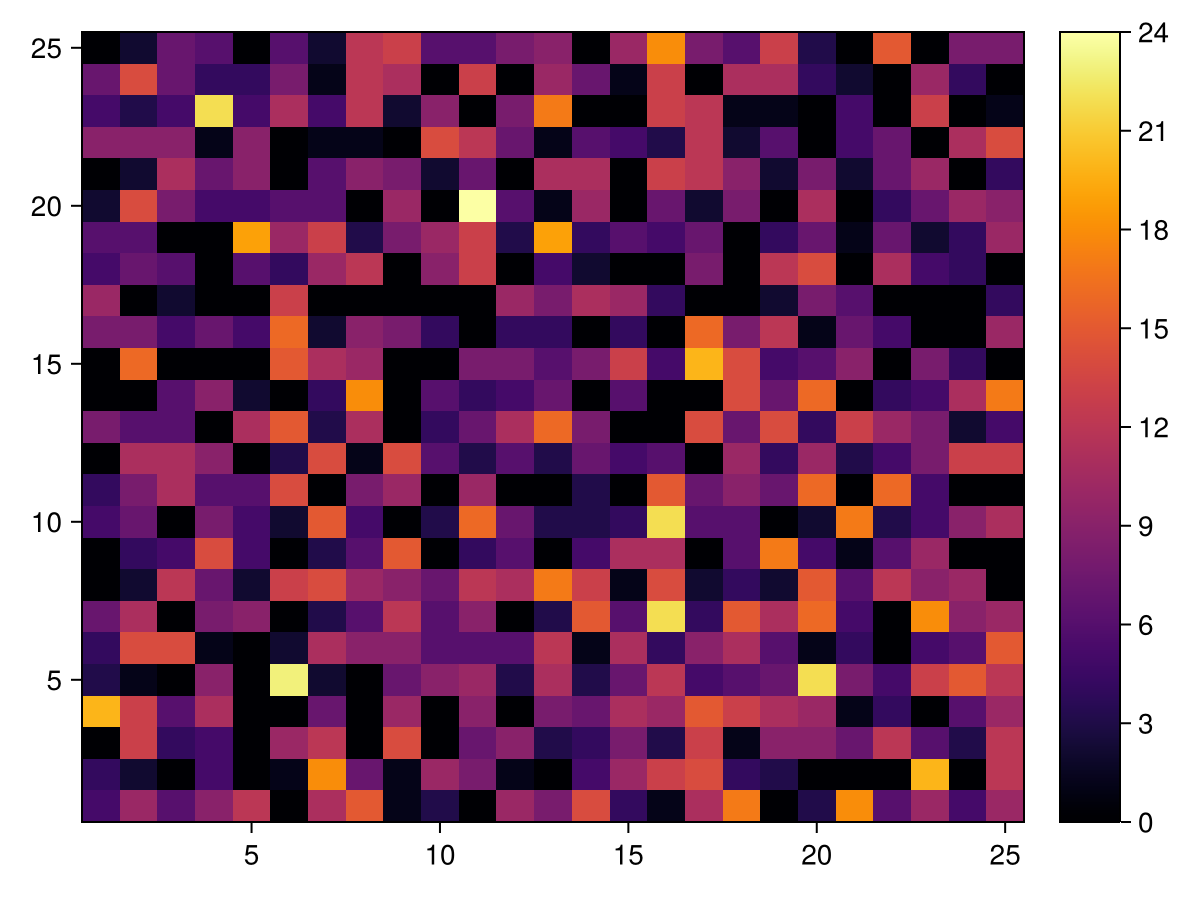

Okay, now we want to get the 2D spatial wealth distribution of the model. That is actually straightforward:

function wealth_distr(data, model, n)

W = zeros(Int, size(abmspace(model)))

for row in eachrow(filter(r -> r.time == n, data)) # iterate over rows at a specific step

W[row.pos...] += row.wealth

end

return W

end

function make_heatmap(W)

figure = Figure(; size = (600, 450))

hmap_l = figure[1, 1] = Axis(figure)

hmap = heatmap!(hmap_l, W; colormap = cgrad(:default))

cbar = figure[1, 2] = Colorbar(figure, hmap; width = 30)

return figure

end

W1 = wealth_distr(data, model2D, 1)

make_heatmap(W1)

W5 = wealth_distr(data, model2D, 5)

make_heatmap(W5)

W10 = wealth_distr(data, model2D, 9)

make_heatmap(W10)

What we see is that wealth gets more and more localized.